What Happens to Your Group Benefits When You Leave a Job?

What Happens to Your Group Benefits When You Leave a Job?

Leaving a job, whether by choice or by circumstance, brings a long to-do list. Updating your resume, signing new paperwork, figuring out your finances. One item that often gets missed in the shuffle: your group benefits.

For many Canadians, employer-provided health, dental, vision, and life insurance coverage quietly disappears the moment they leave. Here is what actually happens, what your options are, and what steps to take so you do not end up without coverage when you need it most.

When Does Coverage End?

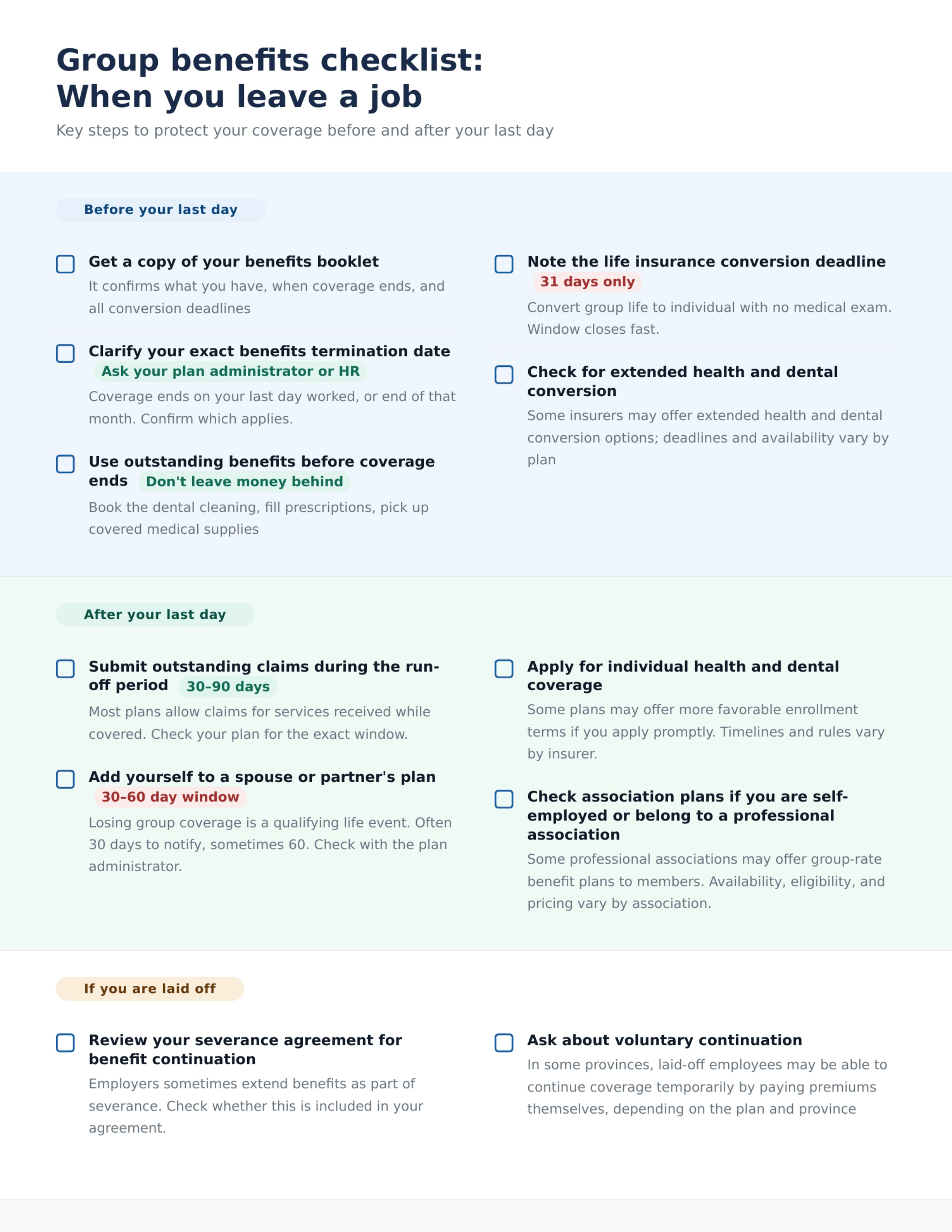

The exact end date depends on your employer’s plan, but most group benefits plans terminate coverage on one of two dates:

-

The last day of active employment, meaning your coverage ends the day you stop working.

-

The last day of the month in which you stop working, which gives you a short buffer.

Your employee handbook or HR contact can confirm which applies to your plan. If you are being laid off or terminated, sometimes an employer will extend benefits for a defined period as part of a severance arrangement, this should be spelled out in any severance agreement you receive. In some provinces, such as British Columbia, employees who are laid off may also have the option to voluntarily continue their coverage for up to six months by paying the premiums themselves.

The takeaway: do not assume coverage continues past your last day. It usually does not, and even a brief gap can leave you on the hook for expenses.

What Coverage Goes With You, and What Disappears

Not all group benefits disappear the same way. Here is what typically happens with each type:

Health and dental: These end on your termination date (or end of month, depending on the plan). Most plans include a run-off period, typically 30 to 90 days, to submit claims for services you received while you were still covered. Any claims for services after your termination date will be denied. Before you leave, it is worth getting any outstanding treatments done and filling any prescriptions. Some insurers also offer conversion options for extended health and dental coverage within 60 to 90 days of losing group coverage, though this is less common than life insurance conversion.

Vision: Same as health and dental, coverage ends, and unused benefit maximums do not transfer.

Life insurance and accidental death and dismemberment (AD&D): Group life insurance through your employer is usually converted to an individual policy without medical evidence through a feature called the conversion privilege. This is one of the most important and least-known options available to departing employees.

Short-term and long-term disability: These stop when employment ends. You cannot claim disability benefits from a former employer’s plan after your last day. If you are already on a disability claim when you leave, the rules get more specific, check your plan documents.

Employee Assistance Programs: These end at termination as well.

The Conversion Privilege: A Rarely Used but Valuable Option

Most group life insurance plans come with a conversion privilege, the right to convert your group life coverage to an individual permanent life insurance policy without providing evidence of insurability. That means no medical questions, no physical exam.

There is a catch: you typically have only 31 days from the date your group coverage ends to exercise this option. Miss that window, and you lose it.

The converted policy will cost more than your group coverage did. Group rates are typically lower because the risk is pooled across all employees. An individual policy reflects your age and the fact that the insurer cannot screen for health. But for someone who has developed a health condition during employment and would otherwise have difficulty qualifying for individual coverage, this option is a lifeline.

Contact your former employer’s benefits administrator or the insurer directly to find out the exact deadline and how to start the conversion process.

Your Options for Replacing Health and Dental Coverage

Once your group plan ends, you have a few paths to replacing health and dental coverage:

A spouse or partner’s plan. If your partner has their own employer plan, losing your group coverage is typically considered a qualifying life event that allows them to add you immediately, without waiting for an open enrollment period. Act within 30 to 60 days of your coverage ending, as most plans require prompt notification.

Individual health and dental insurance. Insurance companies offer individual health and dental plans that you can apply for on your own. Premiums are higher than group rates, and pre-existing conditions may not be covered, but this option fills the gap if no group plan is available to you. Many providers allow applications within 60 days of losing group coverage to waive certain waiting periods.

Professional or industry associations. Some professional groups, engineers, teachers, freelancers, offer group benefit plans to members at better rates than individual plans. If you belong to or qualify for membership in an association, this can be worth exploring.

What to Do Before Your Last Day

A few practical steps to take before you walk out the door:

Get a copy of your benefits booklet or summary plan document. This outlines exactly what your plan covers, how conversion works, and the deadlines involved. HR should be able to provide this.

Use what you can before your coverage ends. Book that dental cleaning, fill outstanding prescriptions, and pick up any medical supplies covered under your plan. Most people leave money on the table simply by not timing this properly.

Clarify your exact termination date for benefits purposes. Ask HR explicitly whether benefits end on your last day worked or at the end of that month.

Check the conversion privilege deadline. If you have any concern about qualifying for individual life insurance, find out your deadline immediately and do not let it pass.

Notify your partner’s employer. If you plan to join your partner’s group plan, they need to notify their plan administrator within the required window, typically 30 to 60 days.

The Gap You Do Not Want

Going without health and dental coverage for even a short time can be expensive. A single dental emergency, a course of prescription medication, or a specialist visit that falls outside provincial coverage can cost hundreds to thousands of dollars out of pocket.

The good news is that a gap does not have to happen. With a bit of planning and quick action after your last day, you can move from one source of coverage to another without interruption.

Have questions about your coverage options? We are here to help. Reach out to our team and we will walk you through what makes sense for your situation.

This content is provided for general informational purposes only. It is not intended to provide investment, tax, or legal advice, and should not be relied upon as such.

Sources: