RDSP Explained

Registered Disability Savings Plan (RDSP) Explained

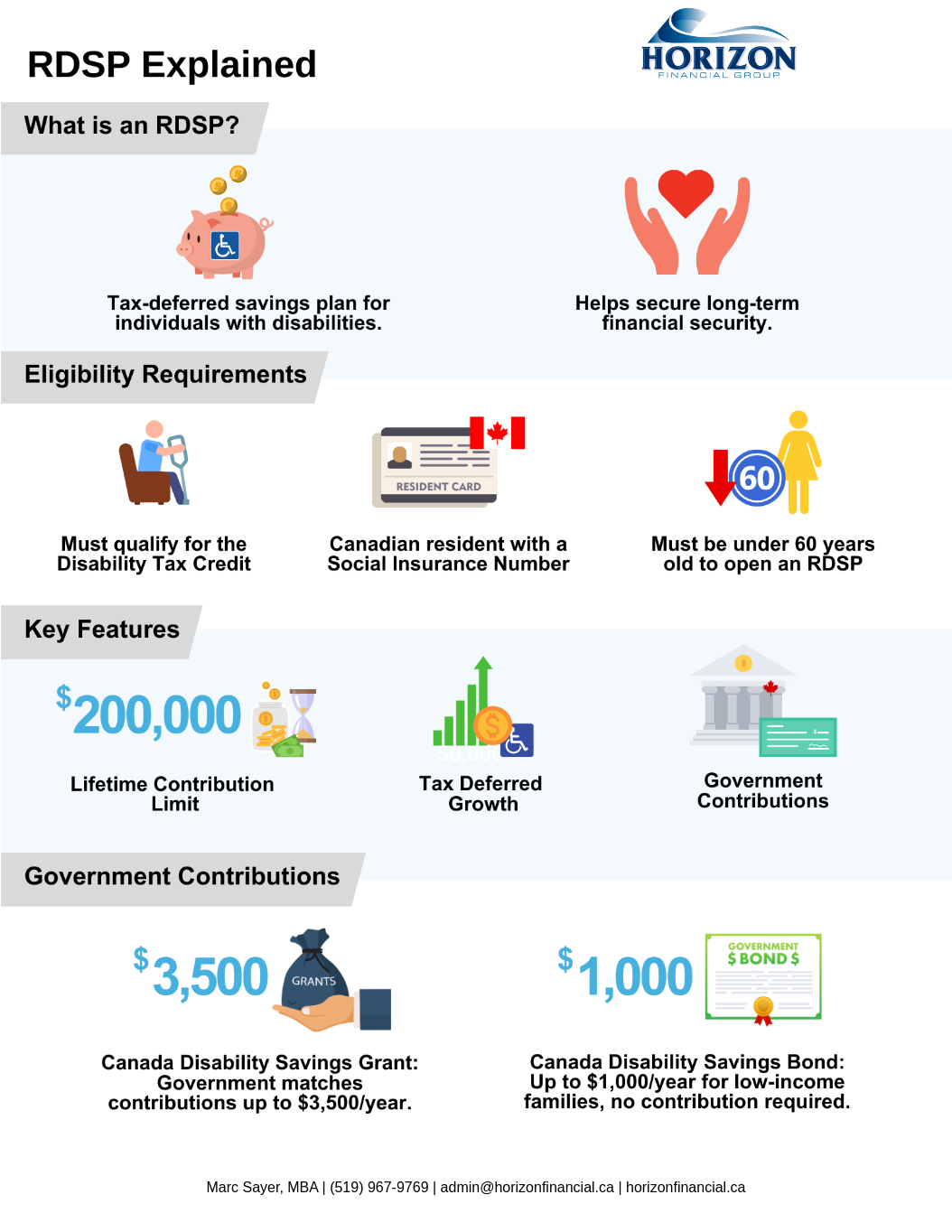

Planning for the future financial security of individuals with disabilities is a priority for many families. The Registered Disability Savings Plan (RDSP) is a valuable tool that offers long-term financial security through tax-deferred savings and government contributions. If you or a loved one qualifies for the Disability Tax Credit (DTC), the RDSP can help build a financial cushion for future needs.

What is the RDSP?

The RDSP is a savings plan designed to help individuals with disabilities save for their long-term financial security. It is a tax-deferred account, which means the investments grow tax-free while inside the plan, though taxes may apply upon withdrawal. The RDSP offers government assistance through the Canada Disability Savings Grant and the Canada Disability Savings Bond, significantly boosting savings for those who qualify.

Key Features of RDSP

– Tax-Deferred Growth: Investments grow without being taxed until withdrawn.

– Government Contributions: Depending on family income, the Canadian government may contribute through matching grants and bonds.

– Flexibility: Contributions can be made by the beneficiary, family, or friends.

– Lifetime Contribution Limit: Up to $200,000 in contributions, with no annual limit.

Eligibility Criteria for RDSP

To be eligible for the RDSP, the beneficiary must:

– Qualify for the Disability Tax Credit (DTC).

– Be a Canadian resident with a valid Social Insurance Number (SIN).

– Be under the age of 60 when the account is opened (contributions cease at 49 years old).

Government Contributions Explained

Canada Disability Savings Grant (CDSG): The government will match contributions up to 300%, 200%, or 100%, depending on the beneficiary’s family income and the contributions made.

For 2023, the income thresholds and matching rates are as follows:

– Family income of $106,717 or less:

• 300% match on the first $500 contributed, giving up to $1,500 in grants.

• 200% match on the next $1,000 contributed, giving up to $2,000 in grants.

– Family income over $106,717:

• 100% match on the first $1,000 contributed, giving up to $1,000 in grants.

The maximum annual CDSG a beneficiary can receive is $3,500, and the lifetime maximum is $70,000. This grant is a powerful tool for enhancing your savings, as the government significantly boosts even modest contributions to the RDSP.

Canada Disability Savings Bond (CDSB) for 2023: The CDSB is available to low-income Canadians to help grow their RDSP even if they are unable to make regular contributions.

For 2023, if the beneficiary’s family income is $37,908 or less, the government will contribute up to $1,000 annually to the RDSP without requiring any personal contributions.

– Families with incomes between $37,908 and $56,756 may receive a partial bond based on a sliding scale.

– The maximum lifetime CDSB contribution is $20,000.

Why Open an RDSP?

The RDSP is one of the most effective ways to save for individuals with disabilities, providing them with long-term financial security. By taking advantage of tax-deferred growth and government contributions, families can ensure that their loved ones have financial support when they need it most.

Contact us today.