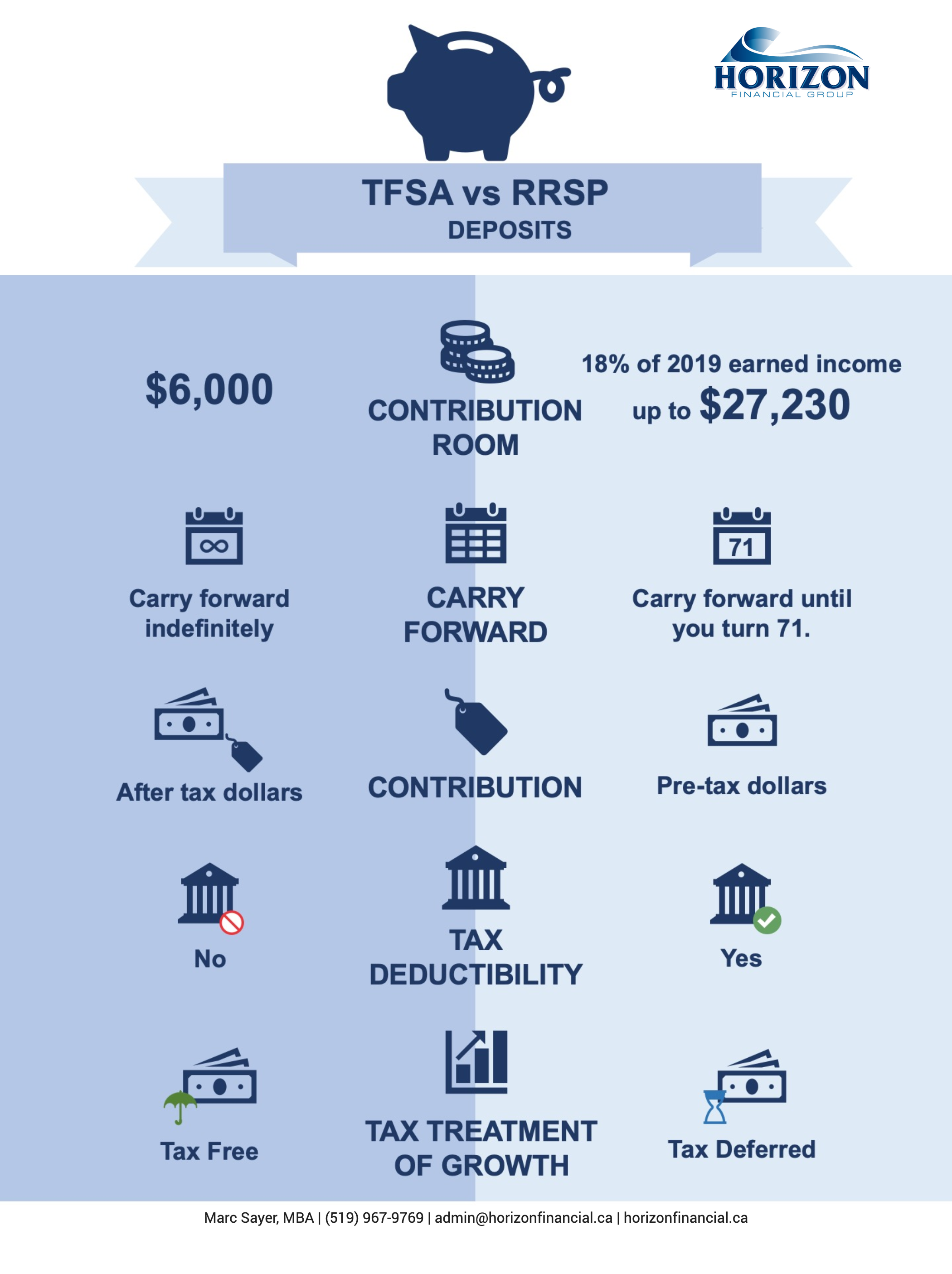

In the Deposit phase, we look at:

-

Contribution Room

-

Carry Forward

-

Contribution

-

Tax Deductibility

-

Tax Treatment of Growth

Contribution Room

TFSA : $6,000 for 2020. If you never opened a TFSA, you can contribute up to $69,500 today.

-

$5,000 for each year from 2009 to 2012;

-

$5,500 for each of 2013 and 2014;

-

$10,000 for 2015;

-

$5,500 for each of 2016, 2017 and 2019

-

$6,000 for each of 2019 and 2020

RRSP : 18% of your 2020 pre-tax earned income or $27,230. So for example if you earned $60,000, then your deduction limit would be $10,800 (18% x $60,000). If you earned $200,000, then your deduction limit would be capped at the max limit of $27,230.

Carry Forward

TFSA : You can carry forward your unused contribution room indefinitely, as long as your a Canadian resident, older than age 18 with a valid social insurance number. Withdrawals will usually result in new contribution room.

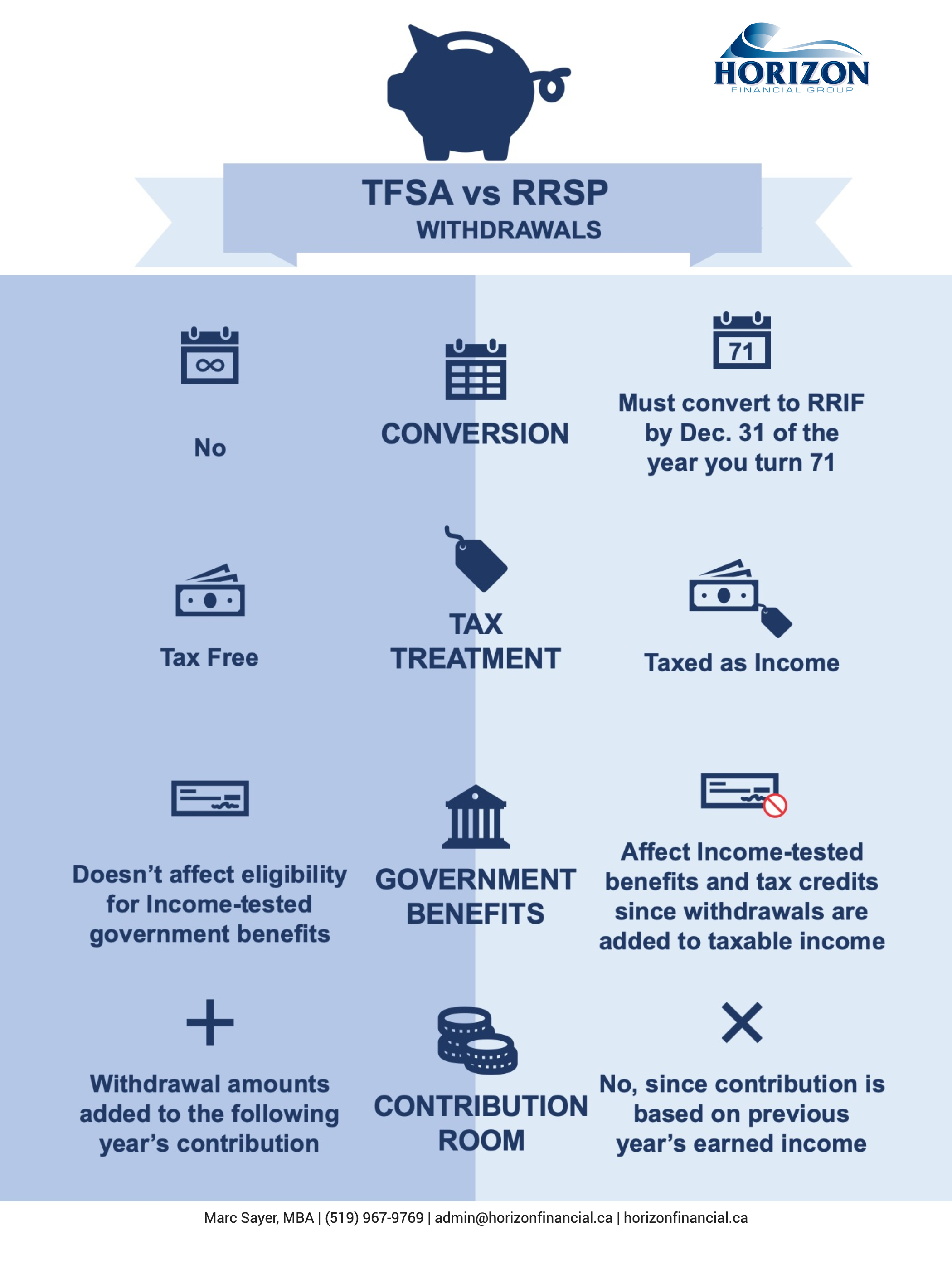

RRSP : You can carry forward your unused contribution room until the age of 71 when you have to convert your RRSP to a RRIF. Any withdrawals made from your RRSP will not result in new contribution room.

Contribution

TFSA : You are contributing to your TFSA with After-tax dollars.

RRSP : You are contributing to your RRSP with Pre-tax dollars.

Tax Deductibility

TFSA : Contributions are not tax deductible.

RRSP : Contributions are tax deductible.

Tax Treatment of Growth

TFSA : The growth inside a TFSA is tax free therefore it’s a great savings vehicle for immediate objectives such as a down payment for a home.

RRSP : The growth inside an RRSP is tax deferred, which means at withdrawal, you will need to pay tax, therefore it’s a good choice for long term goals such as retirement.